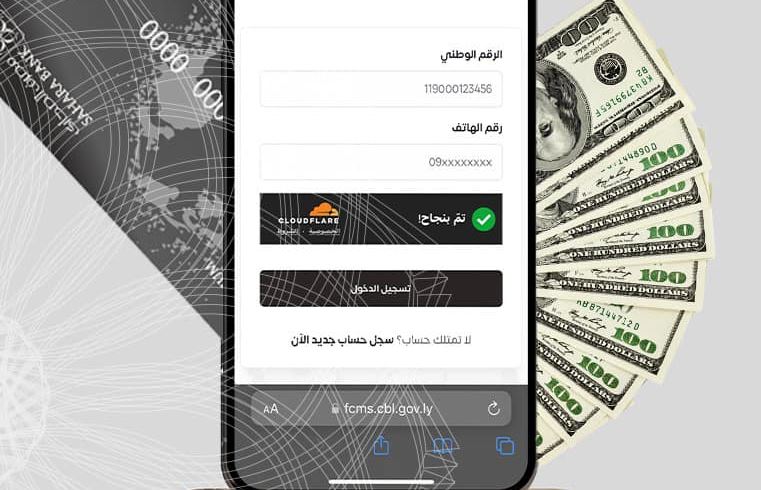

In a statement, Libyan businessman “Husni B” said: Following the Central Bank’s move to link all commercial banks and its three branches in the east, west, and south, along with connecting all electronic payment service providers to the national switch, and the Central Bank’s launch of the “Financial Inclusion” initiative aimed at enabling all residents in Libya to use electronic payment methods; the companies of the “HP” group decided to launch a limited-scale practical trial within the Al-Karimiya market area in Tripoli. In the event of the initiative’s success, it will be extended to cover the entire Libyan market.

He added: This trial has been named “Zero Cash,” and it is based on not accepting paper money in wholesale distribution shops in the Al-Karimiya area initially, to be extended in phases across all of Libya. This step is part of a phased plan spanning six months, culminating in a comprehensive digital transformation by March 31, 2026, with the goal of a complete shift to the digital payment system and the total abandonment of cash transactions.

He continued: The announcement of this initiative in October came as a shock to some, with some meeting it with disbelief, while others moved to adopt, support, and follow the same step.

He also said: This coincided with a severe shortage of paper currency resulting from the implementation of the Central Bank’s decision to withdraw the 20 and 50 Libyan dinar denominations, as part of regulating the money supply and determining the real and effective monetary base, enabling the bank to establish monetary policies based on realistic indicators. This process resulted in a major surprise: the discovery of over 10 billion Libyan dinars of these two denominations from unknown sources, representing about 22% of the total of the two denominations withdrawn during 2025.

He went on: This led to a severe liquidity crisis, resulting in a trend, or rather a necessity, to accelerate towards the use of electronic payment methods. Due to these developments and crises, a decline in reliance on cash payments was observed from rates exceeding 60% until 2023 to below 40% by September 2025. With the launch of the “Zero Cash” initiative in mid-October 2025, we witnessed an unprecedented rise in electronic payment acceptance rates, exceeding 90% in its first phase, then the reliance on cash declined to less than 10%, reaching the achievement of a 100% electronic payment rate this week. Thus, the planned goal was achieved in just nine weeks, instead of the estimated six-month period.

He concluded: Despite this achievement, the level of financial inclusion remains below aspirations, which necessitates accelerating its pace by expanding the use of prepaid cards and allowing the creation of pooled accounts enabling a sponsor to guarantee the users of these cards. This enhances financial inclusion and ensures the sustainability of the digital transformation, particularly in a way that serves the interests of non-resident expatriates, the elderly, and minors.