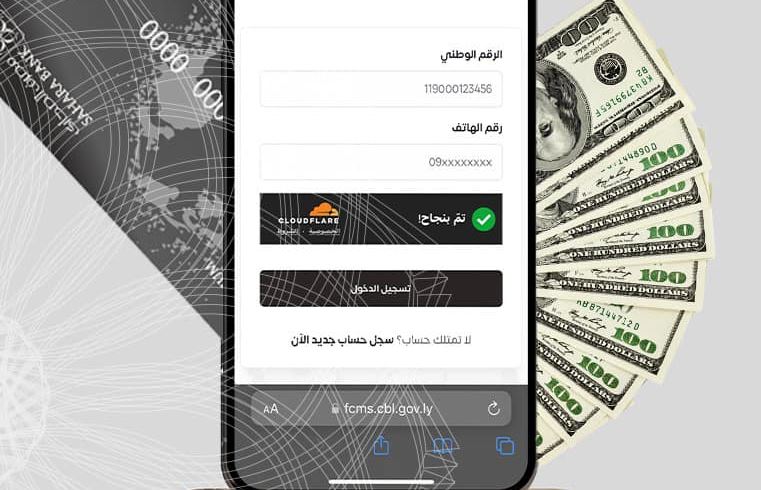

A number of market analysts and influencers believe that the Central Bank of Libya’s decision to activate the sale of foreign currency through exchange offices, despite its importance, still requires deeper institutional treatment to ensure its success and prevent the repetition of past failures.

Analysts confirm that the core issue does not lie with the exchange offices themselves, but rather with a flaw in the current financial cycle related to currency cards. This flaw has spawned a network of intermediaries and high commissions, leading to a significant portion of foreign cash exiting the official banking system and creating a suitable environment for the parallel market to thrive.

Analysts note that citizens are now forced to obtain their allocations through unofficial channels and with high commissions, amid weak oversight and multiple layers of intermediation. This has negatively impacted market transparency and the central bank’s ability to control the movement of foreign currency.

According to analysts, entrusting the foreign currency sales file to exchange offices in its current form carries real risks. The most prominent of these are weak operational readiness in a large number of cities, a lack of qualified personnel, high costs, in addition to weak confidence in the continuity of monetary policies. This could lead to the experiment’s failure at the first wave of complaints or violations.

Analysts believe the practical solution lies in completely re-engineering the financial cycle. This would be achieved by enabling citizens to reserve their allocations electronically and choose an exchange office, with all transfers between banks, exchange offices, and companies conducted within the official banking system with clear commissions. This would ensure the currency remains within the banking system, reduce the role of the parallel market, and separate the citizen from speculation.

Analysts also emphasize that addressing the parallel market cannot be achieved without a direct and effective role for the Central Bank of Libya in managing the exchange rate. This would involve the bank entering the market as an active regulator, pricing the dollar for exchange offices at a rate close to the parallel market while imposing a variable tax whose revenues return to the state treasury, and injecting currency according to supply and demand mechanisms to limit price spikes and speculation.

Financial market analysts conclude by stressing that calls to halt imports except through full bank payment are currently unfeasible, given the limited payment methods and weak operational readiness of banks. They emphasize that eliminating the parallel market is not achieved through administrative decisions alone, but by addressing its real causes, conducting a precise study of the financial cycle, and regulating the roles of banks and exchange offices within a clear and stable monetary policy.